.png?width=2196&height=2196&name=OS%20(1).png)

.svg)

-3.png?width=224&height=213&name=Accelerate%20(2)-3.png)

Knowing how much money a laundromat makes is important, but verifying its expenses is equally important. The important number in a laundromat business, and in any business, is net income—how much money you keep. Failing to account for a laundromat’s expenses can have a devastating impact on your bottom line. This guide walks you through common mistakes to avoid and simple strategies for accurately verifying expenses and protecting your investment.

Common mistakes when verifying expenses

Operating a laundry business is a lucrative venture ripe with opportunities for beginner and seasoned entrepreneurs alike. Once you’ve found a laundromat for sale that fits your criteria, one of the most important steps in the process is verifying its expenses. This will help you decide if it’s a good purchase and allow you to get an accurate picture of its profit potential.

This requires care and diligence—skipping this step can have costly implications for the future of your business. While it may seem straightforward, there are several common mistakes that new buyers make:

-

Missing hidden maintenance costs: Laundromats rely heavily on machinery that needs regular upkeep. Buyers often fail to account for repairs or replacement costs, which can be significant over time.

-

Not considering seasonal utility fluctuations: Utility costs, especially water and electricity, can vary greatly depending on the time of year. Not recognizing these fluctuations can lead to inaccurate expense forecasting.

-

Neglecting property taxes or insurance: These costs can increase over time or vary based on the location. It’s easy to miss factoring in potential increases or assume they are fixed.

-

Failing to account for equipment depreciation: Just like a car fresh off the lot, with each spin cycle, laundry equipment decreases in value. Minimize surprises by factoring in depreciation when conducting an expense analysis.

-

Ignoring labor costs: Of course, there’s a major difference in operating expenses between laundromats with attendants and those without. Some buyers fail to account for wage increases, benefits, or overtime.

-

Overlooking lease terms: The lease may contain hidden costs or clauses that can significantly affect your profitable revenue, like rent increases, shared maintenance fees, or restrictions on business operations.

A Step-by-Step Guide to Accurately Verify a Laundromat’s Expenses

1. Request Bills and Statements

Some expenses are relatively easy to verify, but it’s important not to overlook them in your analysis (which we’ll get to in number 3!). For utilities and other recurring bills, request copies of the actual bills or statements—ideally covering at least two years. This not only provides a baseline for expenses but also reveals any inconsistencies.

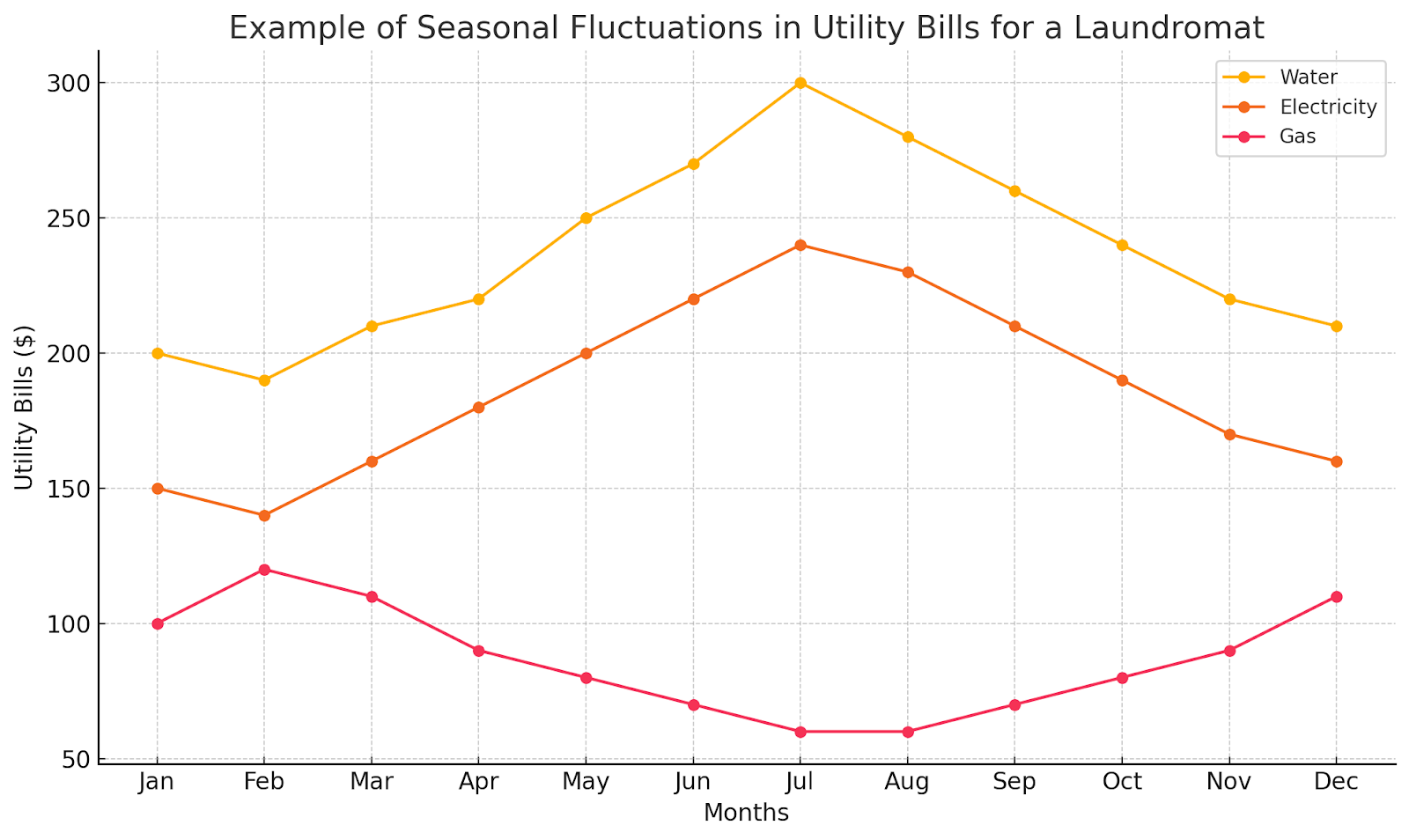

Seasonal Fluctuations of Laundromat Expenses

Utility bills, in particular, offer insights into the business’s performance. Variations in these bills often correlate with fluctuations in the laundromat’s income, helping verify revenue trends. For example, reviewing patterns might show you that income from October through April is higher than from May through September, which is common in some regions. Recognizing these seasonal shifts allows for more informed financial planning.

2. Carefully Review the Lease and All Amendments and Addendums

The lease is the most important document in your business. Your rent plus any common area maintenance (CAM) or triple net costs will be one of your largest expenses. Your financial responsibilities will all be outlined in the lease and documents referred to in the lease (amendments and addendums).

Best Practices in Lease Negotiations

Be sure to look for clauses that could result in higher costs later, such as rent escalations, CAM fees, or repair obligations. Pay close attention to terms that allow the landlord to increase costs unexpectedly, like annual rent increases or shared maintenance expenses. Compile these details and use them to your advantage by negotiating a better deal. For example, you could secure a cap on rent increases or ask the seller to cover certain costs for a certain period after the sale. If you don’t feel confident in your ability to read and negotiate the lease, consider hiring an attorney to help prevent unexpected financial pitfalls.

3. Verify Expenses Using a Pro Forma

One great way to make sure all expenses are accounted for is to use a pro forma. A pro forma will have line items for common laundromat expenses. You can use that to verify that a laundromat's expenses are accounted for.

Not every laundromat will have every expense on a pro forma, but it's worth verifying whether the laundromat you're interested in does or not.

Walkthrough of a Pro Forma

A pro forma is your best friend when verifying expenses. Here’s a breakdown of common line items you should see on it:

-

Rent: Fixed costs tied to the lease agreement.

-

Utilities: Water, electricity, gas, and other key utilities, often fluctuating based on seasonal trends.

-

Maintenance and Repairs: Ongoing equipment maintenance and unexpected repairs are important to consider. Laundry machines, dryers, and HVAC systems require constant upkeep, which add up quickly.

-

Insurance: Necessary coverage to protect the laundromat against risks like fire, theft, or liability claims.

-

Equipment Depreciation: The value of equipment will decrease over time, and it’s important to account for future replacement costs.

-

Supplies: Expenses for detergents, cleaning products, and other consumables required for daily operations.

-

Labor Costs: If your laundromat has staff, account for wages, benefits, and potential overtime.

-

Loan Payments: If you’re planning on financing the laundromat, monthly loan payments should be included to understand the true cost of ownership.

Here’s a typical breakdown of expenses that would appear in your pro forma:

4. Consult an Experienced Expert, Such as Another Laundromat Owner

The more knowledgeable eyes on your deal the better. Tapping into your network of other laundromat owners to get some input on your deal is a great way to analyze the expenses of a laundromat.

Another great tool can be a consultant or coach who has laundromat business experience. There are great consultants out there that could be a great help to you in your laundromat acquisition. One other potential source of consulting could be a broker who is compensated outside of the deal who acts as a consultant and not the broker.

Buy Right the First Time

A huge part of buying right is ensuring you know how much money it takes to run the business so you can have an accurate assessment of the net income you'll keep at the end of each month. Follow the steps outlined above to ensure you do things right the first time! Here's to financial freedom through laundromat ownership.

Book a free demo to see how Cents can help you grow your laundry business and better streamline your overall processes.

.png?width=400&height=200&name=blog%20banner%20(1).png)